It’s cash’s reputation for safety that makes it such a terrible wealth-builder. The bank is not forced to offer a high return in order to attract deposits because people like to hold cash.

Whereas a riskier asset, like an equity ETF, must tempt investors with a much higher potential reward before they’ll part with their money.

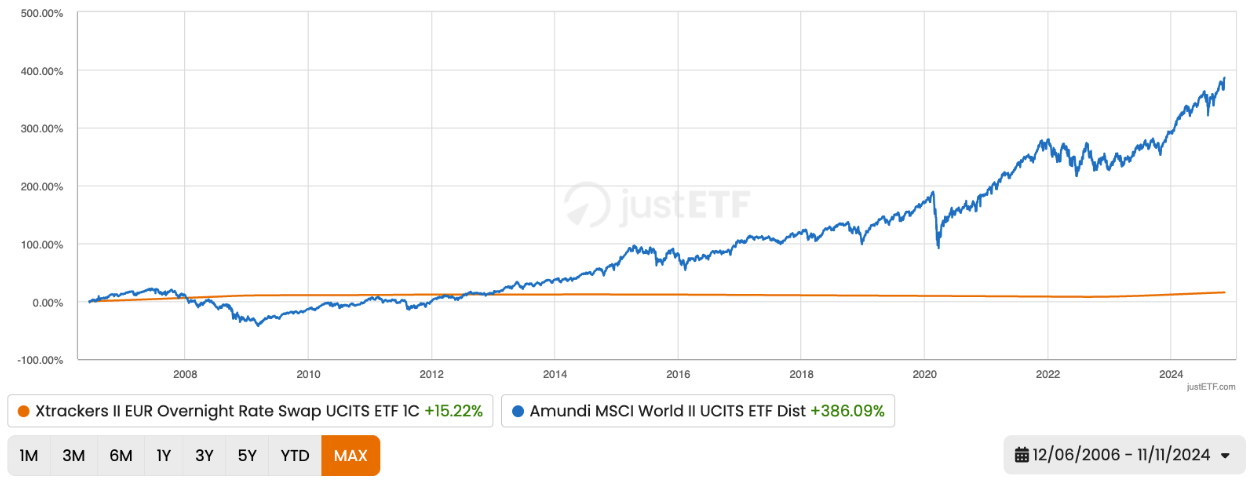

We can see the difference that risk-reward asymmetry makes by comparing cash to a world equities ETF over the past 18 years:

Source: justETF research: 13/11/2024. We’re using a money market ETF (orange line) as a proxy for cash.

Cash (orange line) grew by 15 % overall during this period. In other words, €1,000 would have turned into €1,150 in 18 years.

Meanwhile, equities (blue line) grew by 386 %. So an initial investment of €1,000 would have transformed into €4,860 without any further effort.

You can see from the chart that the cash growth line barely budged. Whereas equities powered upwards, albeit with setbacks along the way. Ironically, the setbacks are central to equities' wealth-building potential.

Mind the gap

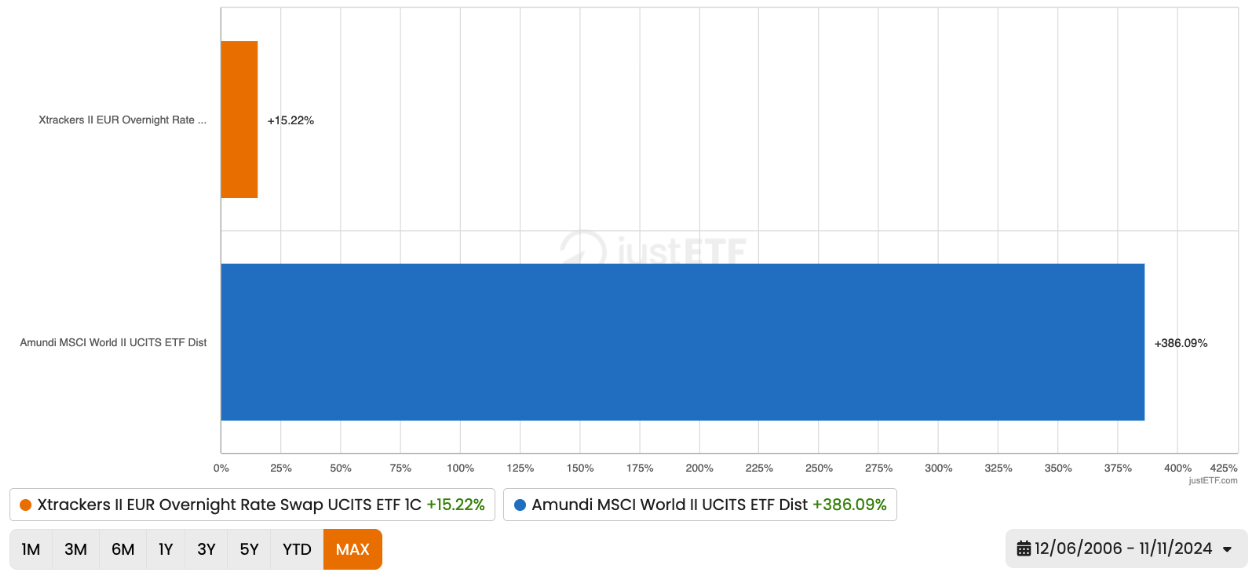

A bar chart vividly illustrates the long-term performance difference:

Source: justETF research: 13/11/2024

The gap in outcomes is stark. Cash delivered a pitiful annualised return of 0.77 % across the period.

Equities on the other hand, brought home 8.96 % annualised.

How long would it take to double your money at those rates?

We can use the Rule of 72 to find out.

72 / 0.77 = 93.5

It would take cash 93.5 years to double your money.

72 / 8.96 = 8

Your money doubles every 8 years if equities can maintain that rate of return.

This is why investing beats your savings account. It’s impossible to grow true wealth just by piling up cash in the bank. (Unless you win the lottery.)

The safety myth

Here’s the real problem with cash. It actually lost purchasing power from 2006 to 2024 due to inflation.

Euro Area inflation averaged around 2 % during our charts’ comparison period. (That period was chosen simply because it’s the longest cash versus equities match-up we can make using ETF data.)

So cash lost 1.23 % annualised after adjusting for inflation. While equities still grew by 6.96 % annualised in real terms.

That’s huge. A 7 % real-terms annual gain is well above the historical average. Whereas wealth stored in cash would have shrunk.

It’s that vulnerability to inflation that makes cash unsafe.

Of course, cash is wonderful for dealing with the here and now. You should always have some savings available to pay the bills and deal with short-term crises like a period of unemployment.

But cash is not suited to the bigger tasks of achieving financial independence or a comfortable retirement.

Role reversal

To be fair to cash, it does not always fare badly against equities.

This time we compare our two ETFs during the 2008-09 Global Financial Crisis - the worst stock market crash of the past twenty years.

Source: justETF research: 13/11/2024

The chart shows that cash and equities were about even for over five tumultuous years.

But the ride was very different.

Equities lost over 50 % in 16 months. Whereas cash trundled on as slow and steady as ever - earning around 1 % annualised.

The MSCI World ETF then spent over four years making up the lost ground before finally overtaking cash on the very last day of this comparison.

We saw what happened next in the very first chart above: equities soared while cash remained flat.

It’s because of events like the Global Financial Crisis that equities are a risky investment. It’s because stock owners may have to bear a large loss, and spend time in recovery mode, that you’re able to earn 8.96 % annualised overall.

And it’s because cash is comparatively stable that it earns a paltry inflation-adjusted return over the long-term.

In short, it’s the risk embedded in equities that makes them so rewarding. You’ll need to weather some storms along the way but, if you do that, then you’ll beat your bank account with investing.

Global ETF investment

Discover the best ETFs on the MSCI World Index in our investment guide!