- Level: For advanced

- Reading time: 10 minutes

What you can expect in this article

Pension systems under pressure

When most people dream of retirement they think of spending more time with the people they love, and doing more of the things they love. But securing the financial freedom to make that dream a reality will inevitably take more resources than the creaking State Pension system can provide. Increasing life expectancy, declining birth rates, and increasing national debt means the State will continue to shift the burden of responsibility onto the individual. Meanwhile company pension schemes have also become less generous in the face of increasing demographic and financial pressures. So it's time to get ahead of the curve and take your future into your own hands. But what is the best way to do this?justETF Tipp: Use ETFs! Exchange-Traded Funds are an easy, transparent, and cost-effective way to achieve your financial goals. You don't need a bank branch or a financial advisor. Though of course, as with any investment, there are risks and nuances to take into account. We explain all below ….

5 ETF advantages at a glance

- Diversification: Instead of pinning your hopes on individual shares, your investment opportunities and risks are spread across many firms. This is a tried and tested method of reducing risk that avoids you banking too much on a single share that plunges in value.

- Low fees: Accumulating assets in ETFs is highly cost-effective. Brokers and ETF providers compete hard on costs and individual investors benefit from the ongoing price war by keeping more of their returns for themselves.

- Buy and hold: Every asset experiences short-term setbacks. The key is to stick to the plan, keep buying when shares are on sale, and then reap the rewards when the stock market recovers and your ETF rebounds in price. The alternative approach of chasing performance and selling assets that have recently performed poorly creates a “buy high, sell low” effect over time.

- The cost-average effect: Let's say you buy 20 shares for 200€ a month. Now the stock market declines by 50% but you keep investing. You’re now able to buy 40 shares a month for 200€. The upshot is, when the market recovers, you own more shares because you kept buying while stocks were cheap. This is the essence of the cost-average effect, and it’s key to making outsized profits over time.

- To take advantage of buy-and-hold, the cost-average effect, and to make sure that you “buy low and sell high,” automate your monthly savings so that you invest a regular amount into your chosen ETFs. Ignore short-term market declines and think of them as an opportunity to pick up some bargains. Remember Warren Buffett’s advice: “Keep buying through thick and thin, and especially through thin.”

- Invest in the best: By investing in equity ETFs like the MSCI World, you are investing in a diverse selection of global companies and will automatically capture the upside of the world’s most profitable stocks.

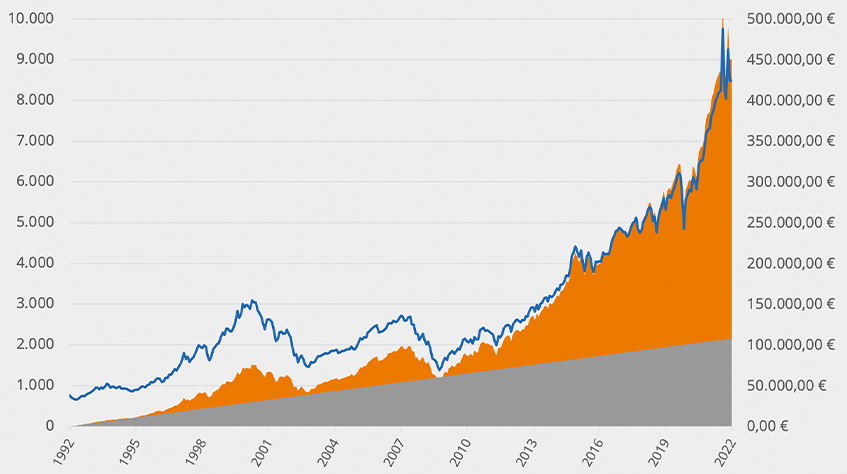

How much money will I have after 30 years of ETF saving?

30-year savings plan simulation, MSCI World EUR, 300€ monthly savings rate

Amount saved (€) Value of units (€) MSCI World (€)

Source: MSCI, "Deutsche Bundesbank", justETF Research; Stand: 31.05.2022

ETF withdrawal strategy: what to look out for

By building up assets outside of State-sponsored or workplace retirement vehicles you can take more control over when you retire and your desired quality of life. Traditional retirement vehicles typically offer advantageous tax breaks but are restrictive in other ways: limiting when you can access your money, how much you can contribute, or how much you can withdraw. On the other hand, amassing a portfolio in a more flexible account can give you the freedom to retire early, at a time of your choosing. An accessible asset base can also help you deal with enforced early retirement scenarios triggered by ill-health or late-career redundancy. Another important consideration is your tax shelter diversification strategy. Traditional retirement vehicles can suffer from adverse rule changes when the government of the day decides to increase taxes. For example, accounts that provide tax relief on contributions but are taxed on withdrawals (tax-deferred accounts) are vulnerable to higher tax rates in the future. Whereas tax shelters that are filled with post-tax contributions now (but don’t impose tax on withdrawals) enable you to lock in today’s tax rates. In short, tax-deferred accounts are liable to be less effective if taxes rise in the future, and more advantageous if taxes fall. The opposite is true for post-tax accounts. Thus diversifying across different types of tax shelters enables you to hedge your future tax exposure.What is the best way to cash out ETFs in retirement?

Safe retirement withdrawal rates are highly personal – there is no one size fits all. Much depends on whether you need your ETF assets to provide an income for the rest of your life. Or whether your portfolio is designed to bridge a gap until your State pension comes on stream. Or perhaps you’re aiming for a lifestyle boost (think round-the-world trips of a lifetime) in the go-go years of retirement. Tax is another complicating factor. Withdrawing too much at once can generate a windfall for the government coffers. Whereas taking a steady income can keep you just under a higher rate tax bracket or enable you to maximise the use of any personal allowances available. Market conditions are also worth thinking about. Liquidating your equities during a crash is always a bad idea. Accumulators can easily avoid this but retirees may be forced sellers if they’re relying on their portfolio for income to pay the bills. Diversification can come to the rescue in this situation. For example, government bonds and gold often spike in value during market slumps. In this scenario, you’d sell your defensive assets at a good price in the bad times. Thus preserving your equities until the recovery takes hold and they command a good price again. Living off your dividends is an ever-popular retirement portfolio withdrawal strategy. By only spending income (and never capital) you guarantee your portfolio will last as long as you do. Plus, it can provide a generous legacy for your heirs. On the other hand, dividend payouts are variable and many people would prefer the stability of a higher, set income that maintains their purchasing power over time. The “4% rule” is the best known rule-of-thumb that seeks to define a stable and sustainable retirement income withdrawal rate. The 4% rule is so-called because it stipulates that a retiree may withdraw 4% of their entire portfolio balance in year one of their retirement.For example:

- Retirement portfolio = 1,000,000€

- Calculation = 1,000,000 x 4%

- Year 1 income = 40,000 €

justETF tip: When you’re ready, you can convert your ETF savings plan into a withdrawal plan. That enables the bulk of your wealth to remain invested while enough of your assets are sold to provide your retirement income. Check your broker’s fees for their services and double-check how taxes are handled. Switch brokers to a retirement-friendly platform if your current option doesn’t provide suitable withdrawal plans for a competitive fee.

In detail: a withdrawal plan over 30 years

We have simulated a historical withdrawal strategy for you. We don't know what the future holds, but in a period that includes its fair share of market pain (including the Dotcom Bust and the Global Financial Crisis), you could have withdrawn significantly more than you paid in – with a comfortable reserve at the end. That's a good indication of what’s possible.- Based on an initial retirement portfolio of 200,000€ in MSCI World shares in 1992, you could have withdrawn an income of 1,200 a month for 30 years. That amounts to a grand total withdrawn of 432,000€.

- Yet thirty years later, by 2022, you would still be sitting on a pot of ETF shares worth over 340,000€!

- An ETF with a management fee of 0.2% would have cost around 15,800€ over this period, plus only 350€ in brokerage fees.

In detail: a withdrawal plan over 20 years

- This time we start withdrawing from our 200,000€ retirement account from 2002. Twenty years later we’ve withdrawn 1,200€ a month – which stacks up to a total withdrawal of 288,000€!

- ETF costs (0.2% management fee) would have totalled around 6,340€ and broker costs (0.99€ per withdrawal) only 236€.

20-year withdrawal plan simulation: MSCI World EUR (Withdrawal rate: 1,000€ per month)

Amount paid out (€) Portfolio value (€) MSCI World in €

Sources: MSCI, Deutsche Bundesbank, justETF Research (31/05/2022)

ETF retirement provision pros and cons

OK, that’s a lot to think about, so let’s sum up with our list of ETF retirement provision pros and cons.Pros

- The chance to benefit from diversification and long-term equity returns

- Low fees (utilise cost-competitive ETF products and dispense with advisor management charges)

- Generates returns even in the withdrawal phase

- The potential to diversify against higher future taxes

- More options to take early retirement and build a fund to guard against unanticipated setbacks later in life

Cons

- No capital guarantee

- Requires personal initiative, plus the ability to manage a withdrawal strategy and to balance the interaction of retirement accounts and the tax system

- Requires discipline

- Potential to exhaust your portfolio prematurely if withdrawal rate too high