From tax cuts to trade wars, discover which stocks might thrive and which could stumble under a second Trump term, and whether you should do anything about it

The potential impact of a second Donald Trump Presidency on stocks has become known as the “Trump Trade”. The Trump Trade attempts to predict the stock market winners and losers should Trump come to power after the November election.

This trade is a thesis based on Trump’s policy announcements, known political positions, past record, and campaign pronouncements as synthesised by analysts, economists, investment firms and the financial media.

Although opinions vary, a broad consensus has emerged, so let’s explore the Trump Trade:

Who are the winners and losers according to this thesis?

Is the trade testable now, even though we don’t know who will win the election?

Should you reposition your portfolio in accordance with the Trump Trade?

All will be revealed!

The stock market winners and losers should Trump win

The Trump Trade thesis predicts:

Regulatory rollbacks and deregulation

Winners: Industries that typically benefit from deregulation, such as fossil fuel extraction and production firms (Trump has vowed to “Drill, baby, drill”), financial services, and certain manufacturing sectors, could see a positive impact on their stock prices.

Companies like ExxonMobil, Chevron, JPMorgan Chase and Goldman Sachs might perform well under a Trump administration due to a focus on reducing regulations that may increase profit margins.

Cryptocurrency firms are another potential winner as Trump has attended crypto fund-raisers, vowed to create a strategic Bitcoin reserve, and chosen a pro-crypto VP pick in JD Vance.

Losers: The renewable energy sector is in the firing line as this industry is liable to suffer from a lack of regulatory support, decreased subsidies and tax credits. Increased international tariffs also negatively impact clean energy firms that are heavily reliant on global supply chains. Environmental regulations might be rolled back, potentially affecting companies committed to sustainability.

Trade policies and tariffs

Winners: US manufacturers and companies that produce goods primarily for the American market could benefit from protectionist policies and tariffs that make imported products more expensive. Trump has proposed a 10 % trade tariff on all non-US goods and muted a punitive 60 % tariff on Chinese imports.

Losers: Emerging Markets suffer during periods of deglobalisation, as exacerbated by protectionist policies such as tariffs. Indeed, the MSCI Emerging Markets index is 25 % Chinese stocks - its largest single country allocation. That said, all non-US firms which export to the States, including European companies, would be negatively impacted if Trump carries out his threat to impose a 10 % universal trade tariff.

Ironically, US companies with substantial exposure to international markets are also threatened. There are three primary effects to consider:

US firms may suffer retaliatory tariffs when exporting to foreign markets.

Many US firms import raw materials, components, semifinished and finished goods from abroad that are liable to attract US tariffs, raising input costs for domestic companies. Apple, General Motors, and Nike are all examples of major US brands which have complex global supply chains that could be disrupted by tariff increases.

US firms whose sales to China are restricted for national security reasons. For example, Nvidia already faces curbs on the type of AI chips it can sell to the Chinese. Eventually, the Chinese market could be closed to Nvidia if China turns exclusively to its domestic supplier.

Additional considerations:

The real risk of Trump’s tariff plan is that it triggers a trade war, tipping the global economy into recession. In that event, stocks as an asset class are liable to tumble in value while investors seek refuge in safe havens like government bonds and gold.

Tax policies and corporate tax cuts

Winners Large multinational corporations that could benefit from lower corporate tax rates and incentives for repatriating overseas cash reserves might see their stock prices increase. Notably, US giants like Microsoft, Alphabet and Johnson & Johnson took this opportunity during Trump’s first term. They used onshored cash to reinvest in their operations or to reward their investors via dividends and share buybacks.

Losers: Smaller companies that don’t have the same level of lobbying power or international operations might not benefit as significantly from these tax cuts, especially if they don't have overseas earnings to repatriate.

Additional considerations:

Trump’s most prominent achievement in his first term was the Tax Cut & Jobs Act (TCJA) which reduced the corporate tax rate and prompted many US firms to bring home overseas profits. The acts provisions are due to expire at the end of 2025 and Trump is likely to prioritise an extension.

However, it’s unlikely that Trump would be able to enact his tax-cutting agenda unless the Republicans make a clean sweep of the Presidency, the Senate and the House of Representatives. That’s because tax reductions must be approved by both chambers of Congress. The Democrats are likely to resist tax cuts to prevent the national deficit from widening - should they retain control of at least one Congressional chamber.

Trade tariffs, on the other hand, can be implemented using the President’s executive powers, making it easier for Trump to carry out that side of his program.

Checks and balances

Before rushing to dump Emerging Markets and load up on a US Financials ETF, we need a sense check:

All sensible political commentators say the race is too close to call. Though Harris has taken a lead in most national polls and the majority of swing states, her current advantage lies within the margin of error. Moreover, opinion polls underestimated Trump’s vote in 2016 and 2020. In other words, this election is likely to go down to the wire, so any move you make is little more than a bet.

We all know there’s a huge gulf between promises made on the campaign trail and the realities that close in once a politician is in office. Trump has form here: he conspicuously failed to follow through on many of his pledges during his first term. What’s more, US Presidents are often stymied by congressional gridlock - though they do have the authority to take unilateral action on trade policy, antitrust and immigration.

Share prices do not dance to the President’s tune. Corporate earnings, a mosaic of macroeconomic forces, and the “animal spirits” of market optimism and pessimism drive stock values - government policy is but one factor in the mix.

We can see the limits of policy expectations upon investment outcomes by comparing the performance of two equity ETFs during Trump’s first term and the Biden era.

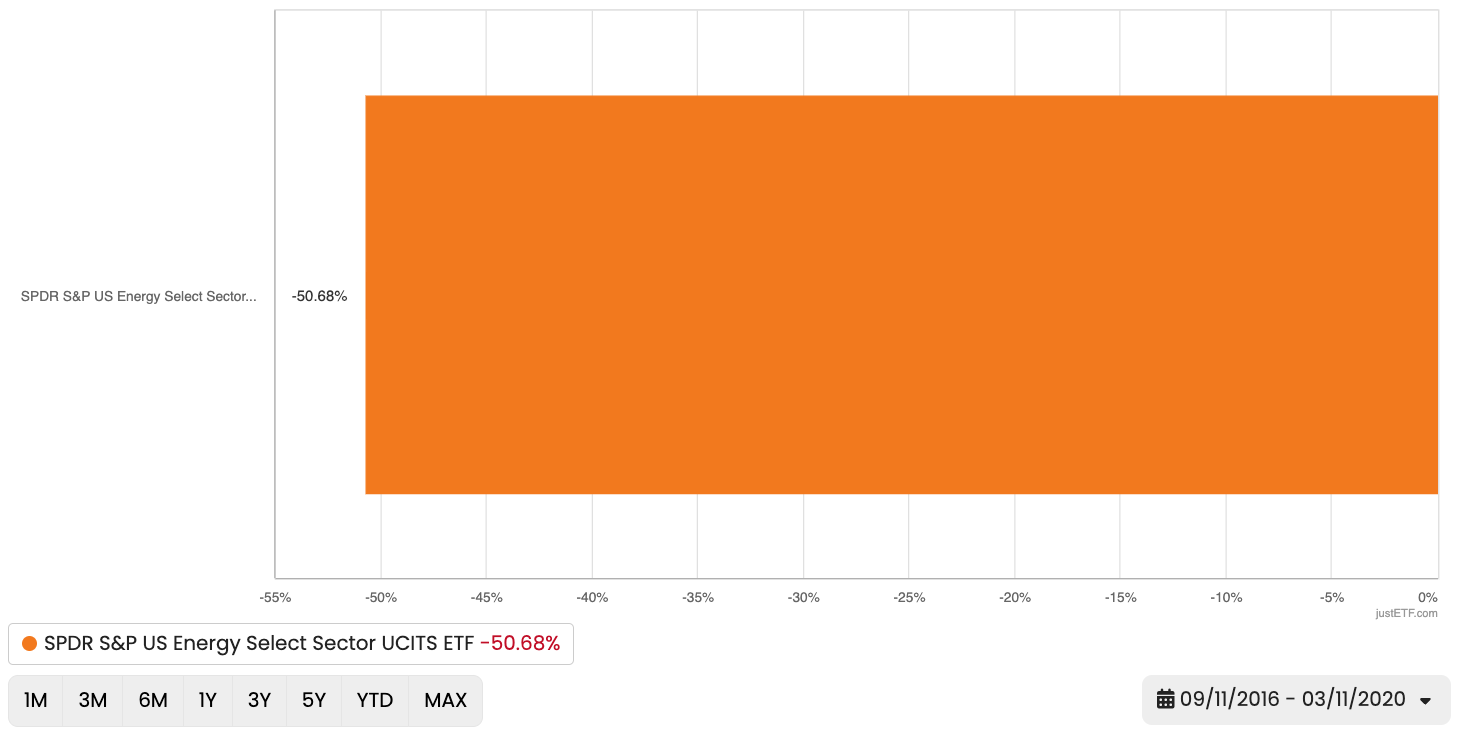

Without the benefit of hindsight, you’d expect Trump’s Presidency to have benefitted US oil and gas stocks more than Biden’s. That didn’t happen:

Source: justETF Research, as of 09/2024

justETF FYI: The S&P US Energy Select Sector Index is dominated by fossil fuel stocks. All results in this article are measured in US dollars, with dividends reinvested.

US energy stocks fell by over 50 % from the day Trump was declared the winner of the 2016 election until the day of the 2020 election.

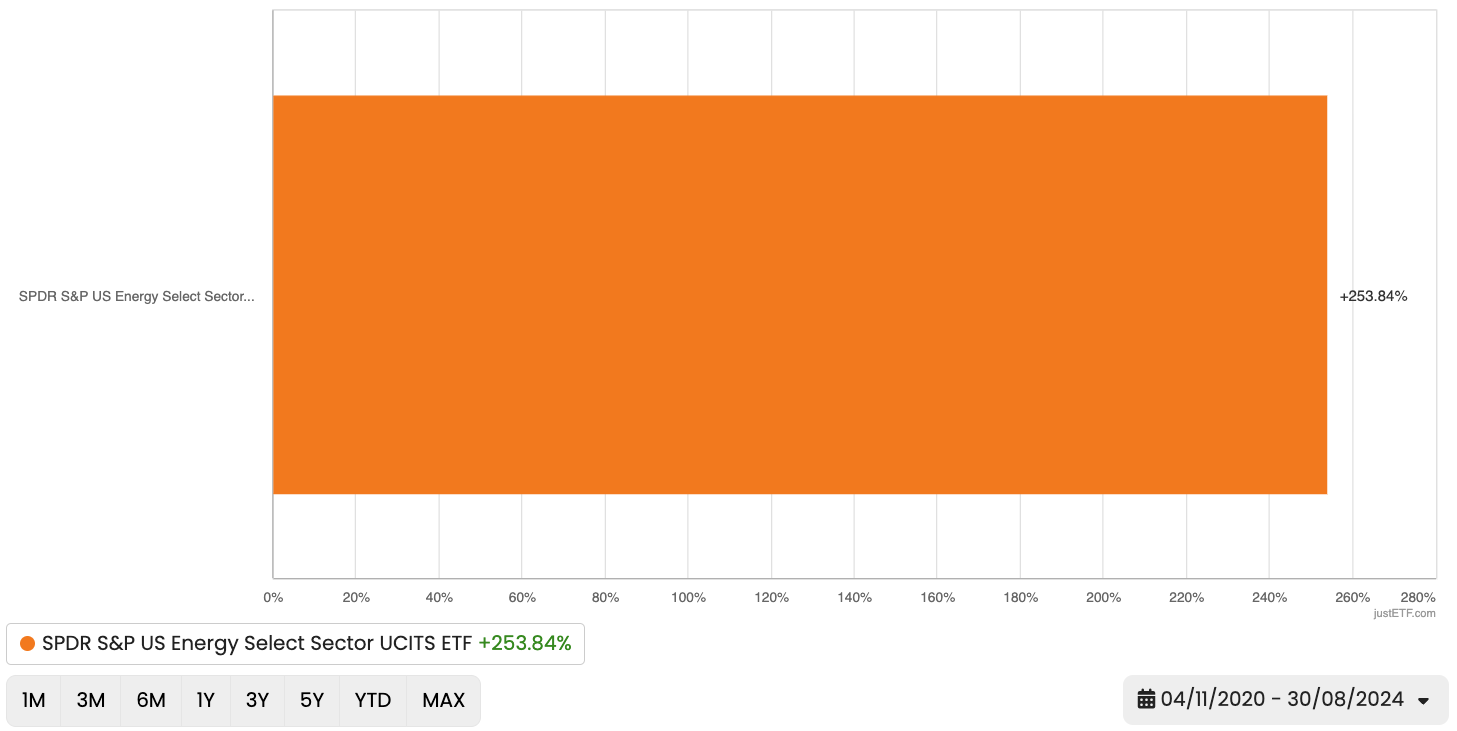

Now check out the performance of US energy stocks during the Biden Presidency:

Source: justETF Research, as of 09/2024

Confoundingly, fossil fuel equities have soared over 250 % under Biden.

The geopolitical impact of the Ukraine War is just one factor that’s proved more important than the apparent political posture of the sitting US president.

Stranger still: the clean energy sector charged ahead under Trump but has fallen back under Biden - despite unprecedented governmental support for renewable energy under his watch.

Testing the Trump Trade

Perhaps the prospect of a Trump victory is moving the markets in 2024, however. We can test the Trump Trade by tracking the performance of sectors which are expected to thrive or dive if the Republican nominee retakes the presidency.

By correlating the results of appropriate ETFs to Trump’s fluctuating campaign fortunes, we can see if there’s any evidence for the Trump effect.

Remember that if the Trump Trade thesis has predictive power, then the lion’s share of the profits will go to the early movers. If you believe that Trump will win - and that will benefit oil and gas shares - then you are better off buying those stocks before other traders bid up the prices, when a Trump win looks all but certain

That truism means that investors who are confident in their analysis, or can afford to be wrong, will act early and rapidly as new information comes to light. This is why the stock market is usually a leading indicator. It’s the lightning translation of news into market moves that makes the stock market incredibly efficient.

So if the Trump Trade is correct, then some investors will buy shares of Trump positive businesses whenever the odds of his victory shorten. Conversely, Trump traders are more likely to trim these same positions if evidence emerges that his campaign is faltering.

So what happened to oil and gas shares when the probability of a Trump Presidency soared in the aftermath of Biden’s stumbling debate performance on 28 June? Did they go up?

Did US energy stocks rise again after Trump’s assassination attempt and during the Republican National Convention as support for Biden drained away?

And have oil and gas shares fallen since Harris was crowned as the Democratic nominee and overtook Trump in the polls?

Because that’s what should be happening if the Trump Trade is worth acting upon…

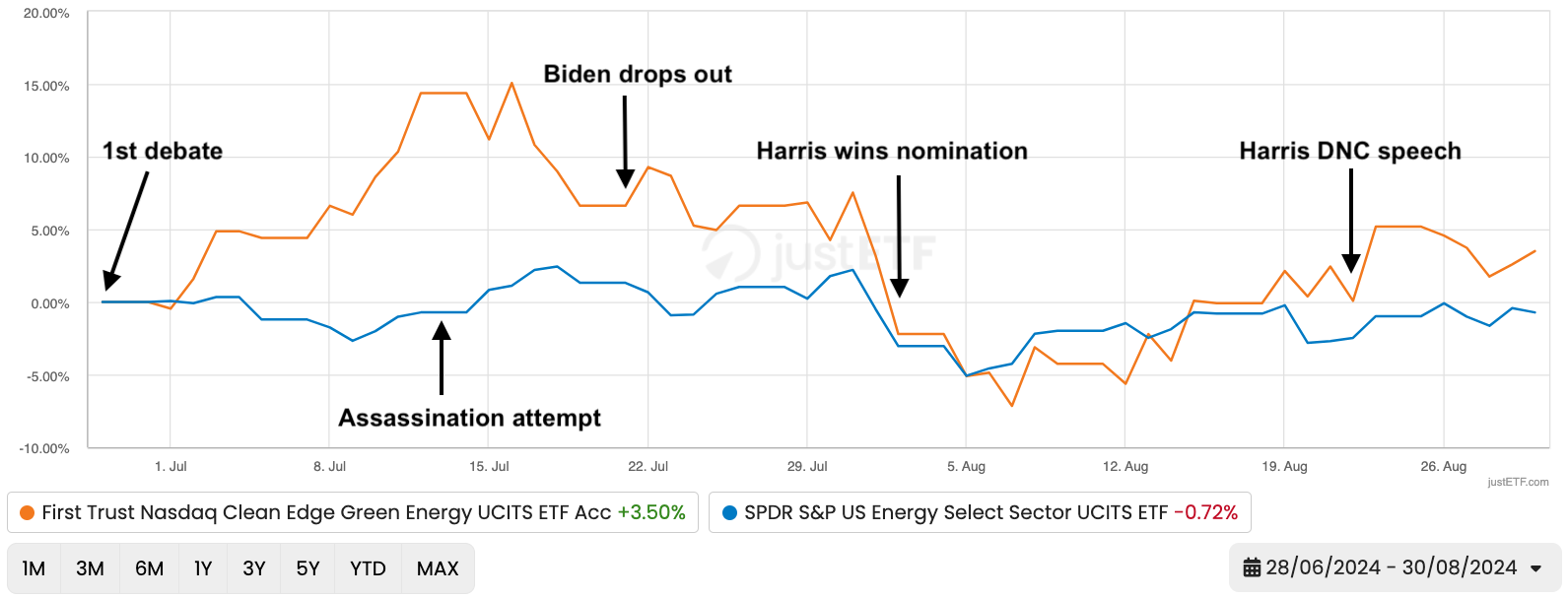

Does the Trump Trade move the market? Fossil fuel vs clean energy ETF check

Source: justETF Research, as of 09/2024

The blue line tracks US fossil fuel stock performance in the guise of the SPDR S&P US Energy Select ETF.

By contrast, the orange line gauges the First Trust Nasdaq Clean Edge Green Energy ETF which is 90 % allocated to US clean energy stocks.

If the Trump Trade is relevant to stock prices, then the clean energy ETF should be negatively correlated with positive news for the Trump campaign, and vice versa for the fossil fuel ETF.

As you can see, the oil and gas dominated ETF slipped slightly after Biden’s frailties were exposed in the first debate. That’s not what we’d expect.

Peak Trump arrives in the aftermath of the assassination attempt and the Republican Convention, held from 15 to 18 July.

Fossil fuel stocks did rise, but it was barely a flicker.

Meanwhile, clean energy stocks were on a tear. They put on 15 % during the two weeks when Biden’s campaign melted down.

Either the market thought the rising prospect of a Trump Presidency was good for clean energy, or other factors were more important.

Biden withdrew his candidacy on 21 July, and the race was transformed. Fossil fuel stocks conspicuously did not go haywire. They continued on a mild downward trend for the next few days.

Indeed, the fortunes of the two ETFs essentially mirrored each other from 22 July to 5 August. They’re highly correlated during this period: as one rises, so does the other. As one falls, so does the other.

At the same time, the Democratic Party was busy anointing Harris as Biden’s successor and reviving their campaign.

But more tellingly, if you overlay a global or S&P 500 ETF onto the chart, you’ll see the broader market was behaving in the same way as the two sector ETFs.

Hence, the performance of the two sector ETFs during that period is better explained by the systematic risks that affect all stocks than by the Trump Trade.

Beyond 5 August, Harris continued to eat into Trump’s poll lead and then overtook him (according to analyses of national poll averages).

We could associate that turnaround with the recovery of the clean energy ETF from its 7 August low.

But in truth, oil and gas stocks were also on a broadly upward trajectory (albeit a flatter one) over the same period, as was the global market.

You can investigate these effects yourself using justETF’s charting tools.

For example, the returns of the iShares MSCI China A ETF show Chinese stocks rising until Biden drops out of the race - then they crater. Again, this is precisely the reverse of the behaviour predicted by the Trump Trade.

Conclusion

We don’t claim our analysis definitively refutes the Trump Trade. But it does suggest that US electoral politics is only one of many influences upon prices, and probably not the dominant one.

US stocks have typically grown regardless of the occupant of the White House.

Occasionally there is a negative era, such as during George W. Bush’s Presidency, blighted as it was by the Dotcom Bust and the Global Financial Crisis. But both those crashes were rooted in economic crises that lay beyond the remit of US presidential control.

So the best advice has to be: ignore the short-term soap opera, stay invested, and maintain a well diversified portfolio aligned to your risk tolerance.

Ultimately, trying to profit from the Trump Trade means:

Correctly guessing the outcome of an election that is currently poised on a knife’s edge.

Correctly guessing what Trump would do in office if he does win. Even Trump probably doesn’t know that.

Correctly guessing how his policies will be altered by Congress.

Correctly guessing how those policies play out in the wider world. Perhaps, for example, the march of US renewable energy is unstoppable because it increasingly offers the lowest cost solutions and individual US states will strive to meet their own climate targets, regardless. Perhaps a trade war will backfire on US industry dependent on global supply chains.

In the face of those odds, few people would make substantial changes to their portfolio with any degree of confidence in the outcome.

Some may build a side position in a particular ETF sector or theme, but only with money they’re prepared to lose. For everyone else, it’s better to keep things simple and stick to your long-term plan.

Global ETF investment

Discover the best ETFs on the MSCI World Index in our investment guide!